IBOR transition

IBOR Reform - current status March 2022

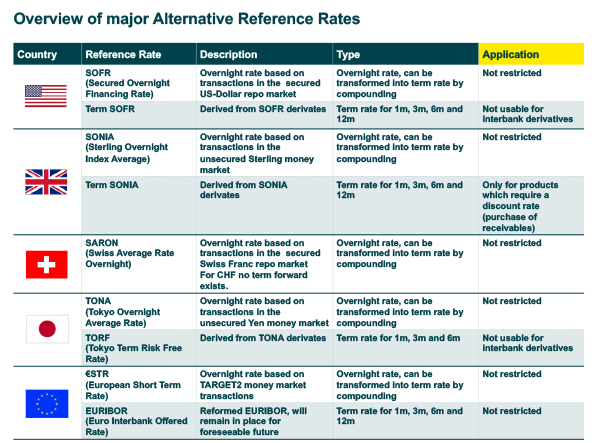

At the end of 2021, the relevant LIBOR reference rates in GBP, JPY and CHF currencies as well as the European overnight interest rate EONIA were discontinued. These rates determined the value of a wide range of financial contracts such as derivatives, bonds, loans, securitisations and deposits. Affected legacy contracts and associated transactions were switched to alternative reference rates. New business in these currencies is only possible in the new reference interest rates, the so-called "risk-free rates" (RFR). For GBP this is SONIA, for JPY TONA, for CHF SARON and for EONIA €STR.

For the USD LIBOR, the quotations for "1 week" and "2 months" maturities were discontinued at the end of the year. The remaining maturities "1 month", "3 months", "6 months" and "12 months" can still be used for existing business until mid-2023. However, as of 01.01.2022, only alternative reference rates such as the SOFR or the TERM SOFR derived from it has to be used for new business.

The EURIBOR can continue to be used in the current, reformed methodology. A replacement by the alternative reference rate €STR is not expected soon.

For the reference rates of other jurisdictions, the development is not yet complete.

A characteristic feature of the new reference rates is the fact that they are determined based on transactions concluded on liquid, secured or unsecured overnight money market transactions in order to ensure the greatest possible transparency, robustness and representativeness.

What are the consequences?

This has the following consequences compared to the previous LIBOR quotation:

- The determination of term rates comparable to LIBOR (for example "3 months") requires a methodology for compounding the daily observed overnight rates (so-called "compounding").

- The fixing rate required to determine the payment amount can no longer be determined at the beginning of the interest peri-od but is only possible at the end of the fixing period (so-called "backward-looking approach").

- The overnight rates and the compounded term rates therefore no longer include the credit risk previously included in LIBOR and the refinancing costs for the respective term. This changes the price calculation of banks compared to the previous LI-BOR quotations.

In some jurisdictions, so-called term rates develop, which are derived from the overnight rates on a forward basis. For example, the SONIA term exists for GBP, the SOFR term for USD and the TORF for JPY. For CHF, no development of such a forward rate is planned. However, the use of these forward rates is partially restricted by regulation. The term SONIA can only be used if the underlying product requires a discount rate (e.g. purchase of receivables). The scope of application of the term SOFR is broader and allows its use in the credit sector. However, in interbank trading, especially with derivatives, the SOFR must be used in compounded form, if necessary.

How Commerzbank supports you in the transformation

Your Commerzbank relationship manager will be happy to advise you on further detailed questions or advise you on your refinancing and support you in finding a suitable and fair financing option under the new framework conditions. If you are affected by the conversion of your existing business, especially with regard to the upcoming conversion of products still based on USD LIBOR, your relationship manager will contact you in good time to discuss how to proceed.

Alternatively, you can send your questions to our IBOR team.

Send us your question by email

As of 31 March 2022

![]()

![]()

![]()